June 2022 Vol. 77 No. 6

Directional Drilling

24th Annual Directional Drilling Survey

By Robert Carpenter, Editor-in-Chief

While never a simple market, the past two years have seen the complexity of horizontal directional drilling (HDD) reach new levels, due to both anticipated and unexpected problems.

For contractors, navigating the world of HDD, 2022 offers a mix of rewards, frustrations and lost opportunities. Yet, most contractors believe they will be able to successfully ride the waves in this ocean of contrasting turbulence and bounty.

The 24th Annual Underground Construction HDD Survey brought not only answers to key questions, but a strong expression of emotions, concerns and excitement about the state of the HDD industry. The research reflects the incredible versatility of HDD, which never ceases to amaze.

The exclusive Underground Construction industry survey was conducted during March and April. It polled contractors and utilities that actively own and operate HDD units to enable a statistical portrayal of a technology that has forever changed the face of utility and pipeline construction.

Dichotomy

The markets for small rigs versus large rigs could not be more different. The larger rigs have historically relied heavily on energy pipeline construction, which flattened out in 2021, while the small rig market is driven by the white-hot fiber-to-the-premises business.

Still, even with funding readily available for fiber projects, market challenges continue to inhibit rapid expansion for many contractors.

“It’s never dull,” deadpanned a Southwest region fiber optic contractor in his survey responses. “Now, when we have money just waiting to be spent, we can’t gear up enough to take advantage of market conditions.”

He was citing the well-documented supply chain issues handicapping virtually all U.S. business since 2021. With billions already being invested for new fiber installation, on May 17 the Biden administration released another $55 billion from the Infrastructure Investment bill dedicated for rural or underserved markets.

However, after two years of pandemic and shortages, the market is struggling to keep up with demand for construction and the equipment necessary to perform the work, not to mention obtaining labor. While microtrenching and a variety of technologies are commonly used to install fiber to homes and businesses, directional drilling is generally preferred, especially in more heavily populated areas, due to speed of installation and social costs. Plus, supply chain issues have also been limiting other types of underground infrastructure equipment.

“We’d buy 10 rigs today if they were available,” complained a mid-Atlantic contractor. “We’re slowly getting rigs but it’s taking months instead of weeks, so we just get further behind.”

Another contractor from the Midwest explained that “it’s not just a rig shortage that’s hurting us. We finally got a new rig but now we’re having trouble getting drill pipe and tools for all our equipment. It’s not as big a delay as the rigs but still, it’s slowing us down.”

A common issue frequently cited by survey respondents was actually a significant problem before the pandemic – lack of skilled workers and a labor force, in general. After the pandemic, the problem still exists at acute levels.

“We’ve been short of people for four or five years now,” said this contractor from the Western U.S. Mountain states region. “We have training programs and bonuses in place and have even worked with a tech school – all that has helped. Still, we are always short of people with too few applying for jobs. It seems to have gotten worse after COVID.”

The good news for the booming fiber business is that supplies and equipment are making their way to the market and purchasing delays are generally expected to slowly ease going into the second half of the year. However, most likely it will be well into 2023 before these issues are more fully resolved. Until then, frustration will continue to plague the small rig drillers.

Another concern is that the fiber installation market is beginning to “get that Wild West feel again,” suggested a West Coast contractor. “I’ve been around for a while and remember back in the late ‘90s during the first big fiber boom. Everybody wanted a piece of the action and contractors with no experience were buying equipment and jumping into the competition, causing lots of problems. We’re seeing that happen again.”

Indeed, concern over “Cowboy Contractors” was raised by several survey respondents citing incidents of new contractors undercutting bids due to inexperience.

“We’ve already been asked to complete a job that somebody else started but couldn’t finish – they were in over their heads,” pointed out this Southwest contractor.

“The good news,” said a Northeast contractor, “is that this time around most owners are sold on HDD, so a bad experience with an inexperienced contractor won’t sour them on HDD in general – just contractors without experience!”

Big rig woes

With the exception of workforce, challenges facing large rig contractors are essentially the polar opposite of the small rig contractors. What amounts to an all-out war on U.S. energy markets has added up to a difficult year for the large HDD market.

Large rig owners’ favorite and historically most reliable market, oil and gas, essentially ground to a halt with the change of politics in January 2021, when Joe Biden was sworn in as president. His “green-energy-at-all-costs” policies have largely been supported by the Democratic Party’s reclaiming of both the House and Senate, which brought a return to a hard left agenda.

While Donald Trump’s policies, in general, were positive for energy, his overall job execution and performance proved divisive across the country as a whole, thus dooming his opportunity for re-election.

Consequently, when Joe Biden and the new Congress took office, the writing was on the wall. One of Biden’s first acts was to block the Keystone XL Pipeline. His policies and appointees have largely followed a program of confining and shrinking oil and gas energy, while forcibly supporting alternative energy programs.

The result has predictably caused extreme spikes in oil and gas prices, virtually no exploration and production for new fields and, of course, very little pipeline construction work. Other political and market factors have also tended to blunt any growth in oil and gas supplies. These include aggressive legal tactics from anti-carbon organizations combined with intense pressure on American business to endorse the green energy movement.

Consequently, Wall Street investors have largely turned away from energy companies. Now, with the price of energy hitting record highs, many energy firms are content to pay off debt and increase investor dividends. Of course, with high energy prices, suddenly the roar of green energy is not quite as loud and energy companies are rapidly becoming attractive investments.

No one really is buying President Biden’s rhetoric blaming Russian President Vladimir Putin for the energy price increase. Prices were skyrocketing long before Russia invaded the Ukraine. Only a small part of the 500,000 barrels of Russian oil the U.S. was importing went to fuel production, and in overall U.S. consumption, it was a drop in the bucket.

With the government supporting anti-pipeline forces, the likelihood of a significant increase in pipeline projects anytime soon is slim. For now, major projects are few and largely relegated to intrastate and minor jobs, leaving the existing pipeline infrastructure to carry the load.

With incentives removed, green lawsuits lined up. Viewed favorably by the current administration and its backers, it’s hard to blame energy companies for moving slowly, rewarding shareholders, and seeing what tomorrow will bring. Even should opportunities re-emerge soon, the new regulatory burdens and hurdles will slow the growth of pipelines.

Changing tides

The good news for pipelines is that the political pendulum is beginning to swing back towards supporting the industry. With fuel prices at record highs and inflation out of control, pressure continues to amass against current politics inhibiting traditional oil and gas markets.

To further add complexity and concern to the situation, President Biden has continuously been raiding the national strategic petroleum reserves, expecting it to ease high fuel costs, but to little or no effect. The result is that now our reserves are also at low levels, without much hope of being replenished anytime soon.

Moderate Democrats and Republicans are both clamoring for action by the Biden Administration to address these issues, as the energy crisis drags on.

A veteran large rig owner from the Southwest had an interesting take on the situation.

“I’ve been in this market for over 40 years and weathered plenty of tough times,” he observed. “But never have we had such a rough stretch when the price of oil and gas are setting records! You would expect our markets to be booming.”

A veteran driller from the Midwest related an amusing story.

“Last year we were drilling a gas pipeline crossing. There were a few protestors for a couple of days. One yelled at me that we should be using green hydrogen instead of gas. I yelled back ‘that’s fine with us – hydrogen still needs to be transported in a pipeline!’ The guy frowned and turned away. These people don’t understand the nature of energy.”

Other markets

Another aspect of the Infrastructure Bill that could impact underground utilities and, specifically, HDD is the $65 billion dedicated to the “hardening” of the power grid, ostensibly to better absorb weather extremes and reduce mass outages.

Small rig directional drilling has become a common tool for installation of distribution electric lines and in recent years, there has been a steady swing towards placing transmission lines underground via mid- to large-size HDD rigs.

The technology to place these transmission lines underground has steadily improved to the point that many utilities, increasingly under pressure to do away with the eyesores, continuous maintenance and inefficiencies of electric transmission towers, have started examining new construction options.

HDD has slowly gained favor, albeit still more expensive due to the requirement of heat-shedding thermal grouts and conduits. Still, the cost discrepancy between overhead versus underground continues to shrink, making HDD more practical.

While hardening of the electric grid can encompass many options, simply going underground with both new and established distribution and transmission lines is the preferred choice for longevity, reduced maintenance and aesthetics by most power utilities, when funds are available.

It’s unknown at this time how much of the $65 billion will be spent moving electric grids underground, but most experts expect it to be substantial. This could whip up the small rig market even more, but also provide work for the beleaguered big rig market.

The water market continues to grow and so does the use of HDD, offering mid and large rigs multiple project opportunities. While most large directional drilling companies are accustomed to working with private industry (i.e., oil and gas firms) and prefer not to engage in the public works market. organizations such as municipal water agencies offer prospects that are sorely needed. Plus, HDD use for water installations is projected to be a lucrative market for some time.

“While we still prefer working in the oil and gas industry (for pipelines), we are doing quite a lot of water drilling,” said this Midwestern contractor. “It’s different than working for gas companies and has its own separate slate of challenges. But it’s keeping us reasonably busy for now. In fact, even when pipelines come back, we’ll probably try to keep doing a certain amount of water jobs.”

Qualities

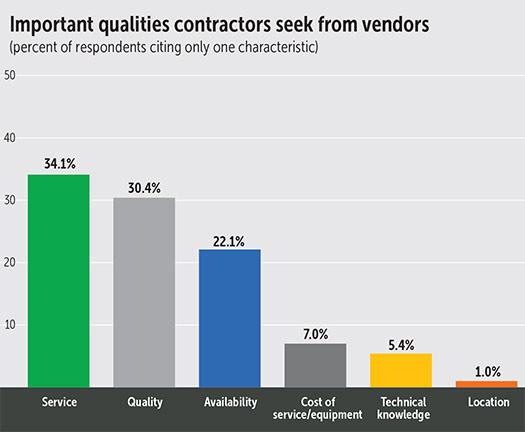

The survey also historically asks contractors about the most important qualities they seek from their manufacturer and supplier partners. Typically, service and quality are by far the strongest responses.

While those two categories are still the most popular (34.1 and 30.4 percent, respectively), “availability” took a huge jump this year, to 22.1 percent. With access to equipment and supplies now a slow process, contractors see it as a top factor.

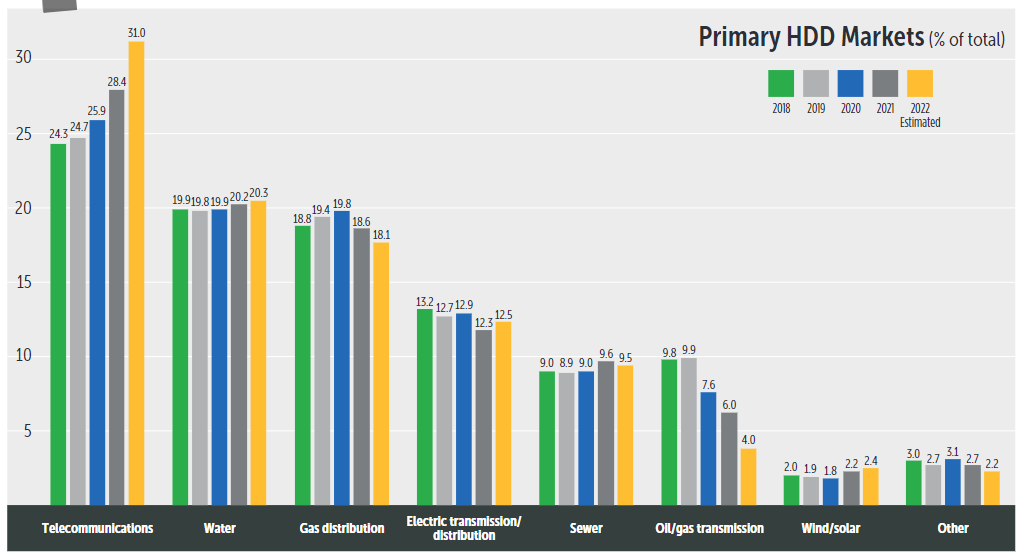

Even with the slowdowns in HDD rigs and equipment, telecommunications (essentially fiber) remains the largest market segment by a substantial margin, at 31.0 percent. Water, at 20.3 percent, continues to embrace HDD, thanks to various pipe types adapting as well. Gas distribution fell to 18.1 percent market share. Not surprisingly, major energy pipeline work has fallen to roughly 4 percent of the market.

When asked about future prospects for the continued growth of HDD, most respondents strongly agreed the technology has a bright future, despite the challenges of today.

“There’s no doubt HDD will remain a strong part of how we work every day,” pointed out a West Coast contractor. From the Northeast, this contractor proclaimed, “our company couldn’t begin to take on half the projects we do without HDD being a huge part of the project.”

Mud disposal of drilling fluid remains a major issue for many contractors and was again referenced frequently in the survey comments.

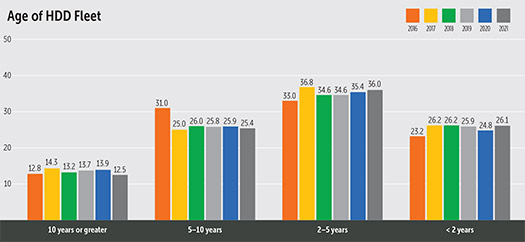

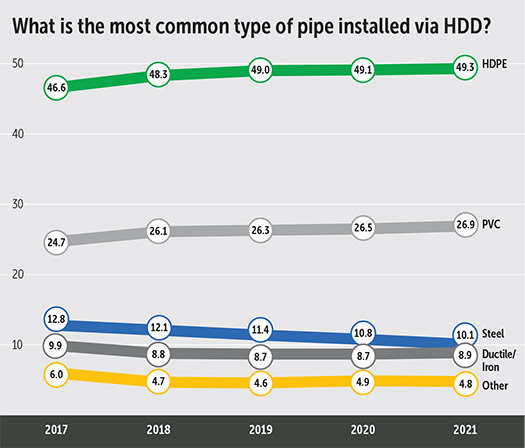

With the expansion of the fiber market over the past few years, it’s no surprise that the average age of a contractor’s HDD rig fleet decreased in 2021. Rigs 10 years and older comprise about 12.5 percent of active units. Rigs two to five years old comprise the largest market segment, at 36 percent, and 26.1 percent of small rigs are under two years old. The most common pipe installed via HDD remains HDPE, with a 49.3-percent market share, while PVC follows at 26.9 percent.

Original equipment manufacturers (OEMs) in the HDD tooling and drill pipe sectors play a vital role with many contractors. About 43.6 percent of downhole tooling is purchased from OEMs and 48.8 percent of drill pipe.

Comments